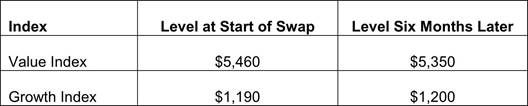

A portfolio manager enters into an equity swap with a swap dealer. The portfolio manager agrees to pay the return on the Value Index and receive the return on the Growth Index. The swap's notional principal is $50 million, and the payments will be made semi-annually. The levels of the equity indices are as follows:

The net amountowedtothe portfolio manager aftersix monthsis closest to:

A.$1,427,494.

B.$1,007,326.

C.$587,158.

参考答案与解析:

-

相关试题

-

A portfolio manager enters into an equity swap with a swap dealer. The portfolio manager agrees to p

-

[单选题]A portfolio manager enters into an equity swap with a swap dealer. The port

- 查看答案

-

Florence Zuelekha, CFA, is an equity portfolio manager at Grid Equity Management (GEM), a firm speci

-

[单选题]Florence Zuelekha, CFA, is an equity portfolio manager at Grid Equity Manag

- 查看答案

-

An equity fund manager is considering a market index as benchmark for his portfolio and he has the f

-

[单选题]An equity fund manager is considering a market index as benchmark for his p

- 查看答案

-

An equity portfolio manager is evaluating her sector allocation strategy for the upcoming year. She

-

[单选题]An equity portfolio manager is evaluating her sector allocation strategy fo

- 查看答案

-

Danielle Deschutes, CFA, is a portfolio manager who is part of a 10-person team that manages equity

-

[单选题]Danielle Deschutes, CFA, is a portfolio manager who is part of a 10-person

- 查看答案

-

Kam Bergeron, CFA, is an equity portfolio manager who often takes time off in the afternoon to play

-

[单选题]Kam Bergeron, CFA, is an equity portfolio manager who often takes time off

- 查看答案

-

Danielle Deschutes, CFA, is a portfolio manager who is part of a 10-person team that manages equity

-

[单选题]Danielle Deschutes, CFA, is a portfolio manager who is part of a 10-person

- 查看答案

-

A portfolio manager decides to temporarily invest more of a portfolio in equities than the investmen

-

[单选题]A portfolio manager decides to temporarily invest more of a portfolio in eq

- 查看答案

-

A portfolio manager decides to temporarily invest more of a portfolio in equities than the investmen

-

[单选题]A portfolio manager decides to temporarily invest more of a portfolio in eq

- 查看答案

-

A portfolio manager generated a rate of return of 15.5% on a portfolio with beta of 2. If the risk-f

-

[单选题]A portfolio manager generated a rate of return of 15.5% on a portfolio with

- 查看答案